MACROECONOMY & END-USE MARKETS

Running tab of macro indicators: 13 out of 20

The number of new jobless claims rose by 6,000 to 223,000 during the week ending January 18. Continuing claims increased by 46,000 to 1.899 million, and the insured unemployment rate for the week ending January 11 was unchanged at 1.2%.

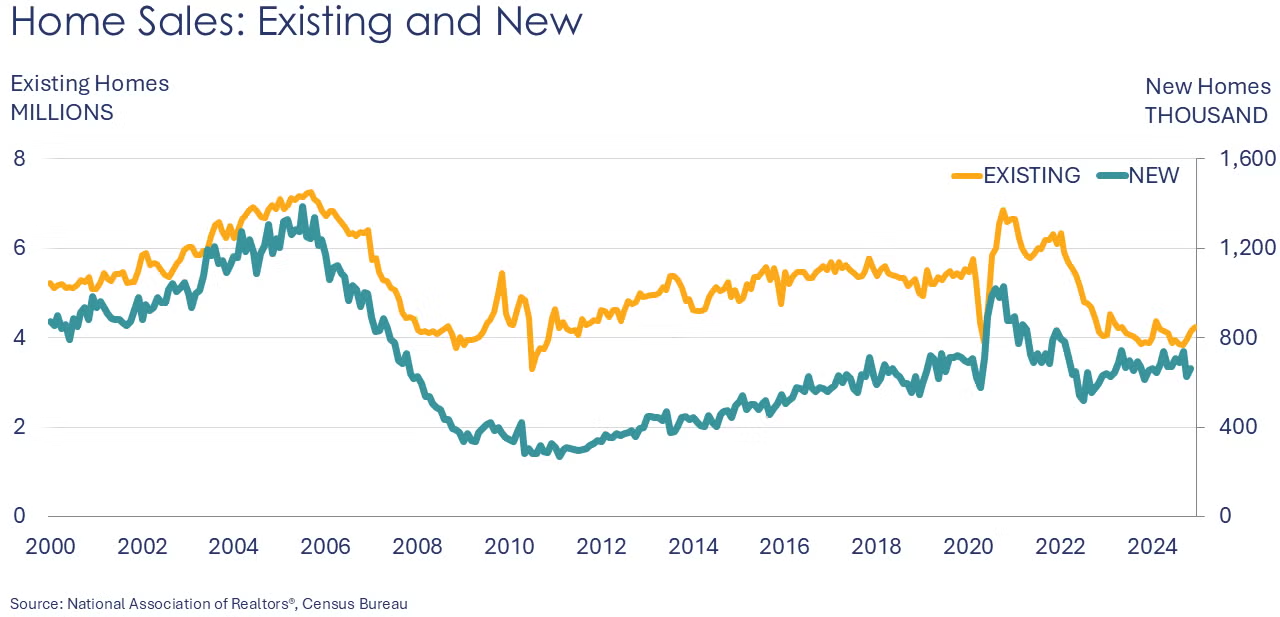

With December data in from the National Association of Realtors (NAR), it looks like existing home sales were pretty much stuck over 2024 (at a roughly 4.1-million-unit pace, about the same as 2023). For perspective, that’s around the low that was hit during the Global Financial Crisis. Elevated mortgage rates continue to challenge the market. There were signs of movement as the year finished up, however. Despite it being the traditionally slower home sales season, existing home sales rose 2.2% in December and were 9.3% higher Y/Y. It was the largest Y/Y gain since mid-2021 when sales jumped to a 23% Y/Y comparison. Inventories were down 13.5% at the end of December (compared to November) and represented a 3.8-month supply. This was down slightly from 3.9 months in November, but higher than the 3.6 months of inventory a year ago. The median existing-home price was up 6.0% Y/Y to $404,400. The median home sales price has risen for 18 months straight.

The Conference Board’s Leading Economic Index® eased by 0.1% in December, following an upwardly revised 0.4% gain in November. Over the past six months, the LEI was 1.3% lower, a slightly slower pace of decline compared to the first half of the year. In December, lower consumer expectations and new orders were the main contributors to the decline.

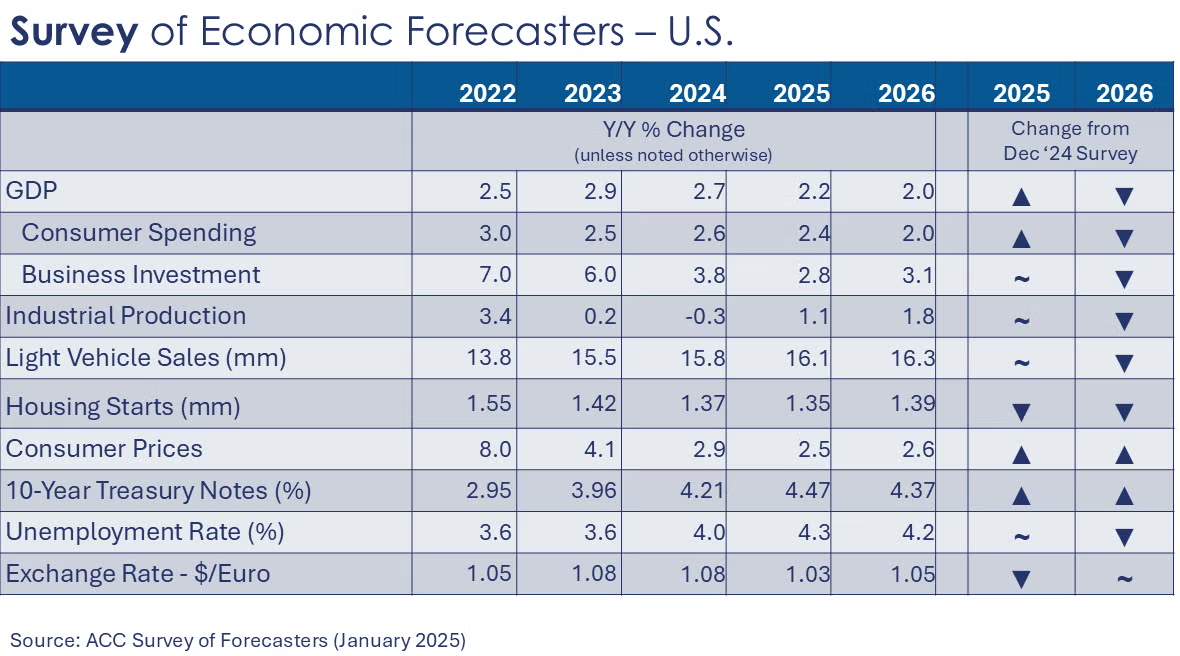

Survey of Economic Forecasters

The U.S. economy is relatively healthy at the start of the new year and expectations for 2025 have improved across many indicators, though expectations for 2026 were a bit lower.

- Current consensus for U.S. GDP is for 2.2% growth in 2025 and 2.0% in 2026.

- Growth in consumer spending is expected to moderate to a 2.4% pace in 2025 before easing slightly to a 2.0% gain in 2026.

- Business investment growth is expected to slow to 2.8% in 2025 before rising to a 3.1% pace in 2026.

- Following a 0.3% decline in 2024, we look for industrial production to expand by 1.1% in 2025 and 1.8% in 2026. Growth is uneven among industries, however.

- Sales of autos and light trucks improved to a 15.8 million pace in 2024 (still below trend, however). In 2025, vehicle sales are expected to rise to a 16.1 million pace and rise further to 16.3 million in 2026.

- Housing expectations for 2025 were revised lower. Housing starts fell to1.37 million in 2024 and are expected to continue to slide in 2025 (to 1.35 million) as pressure remains on the 10-year Treasury which is tied more closely to mortgage rates. A slight improvement is expected in 2026 with housing starts rising to 1.39 million.

- The unemployment rate is expected to move higher as the labor market rebalances averaging 4.3% in 2025 and 4.2% in 2026.

- Recent data continues to show slow progress on inflation. In 2024, growth in the CPI slowed to 2.9%. Growth in consumer prices is expected to slow further to a 2.5% pace in 2025 and 2.6% in 2026 (up from the December survey).

- Despite three rate cuts in 2024, the Fed has signaled “higher for longer”. Expectations for the 10-year Treasury continue to move lower, but at a slower pace.

ENERGY

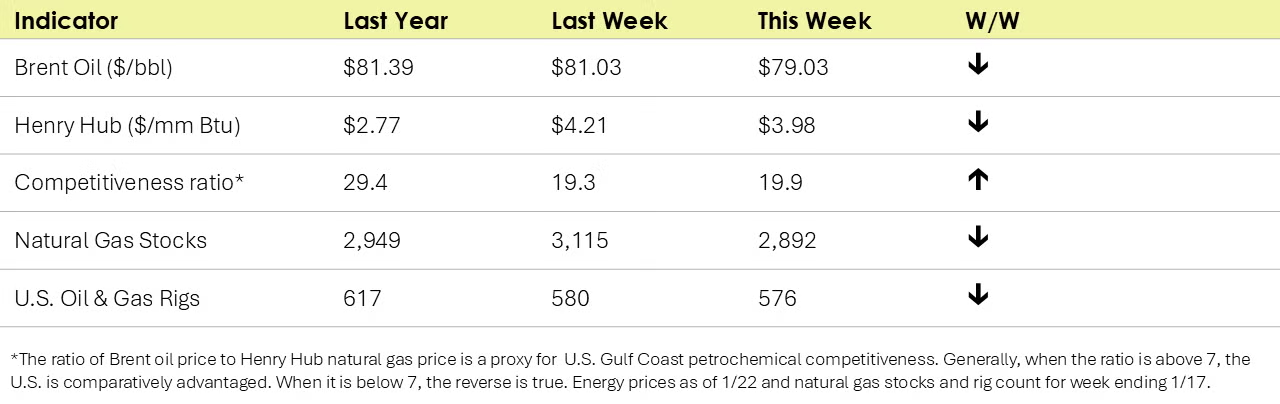

- Oil prices were lower than last week following the Trump administration’s actions to boost energy production.

- U.S. natural gas prices also eased following this week’s cold snap but remain close to $4/mmbtu.

- Natural gas stocks eased.

- The combined oil and gas rig count fell for a second consecutive week, down by four to 576, its lowest level in more than three years.

CHEMICALS

Indicators for the business of chemistry suggest a yellow banner.

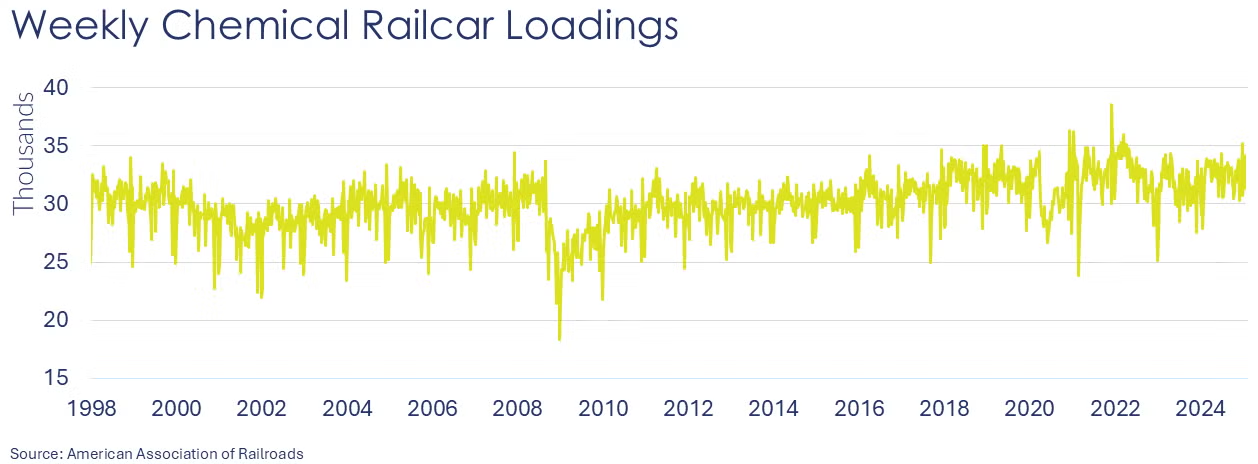

According to data released by the Association of American Railroads, chemical railcar loadings were up to 34,150 for the week ending January 18. Loadings were up 4.5% Y/Y (13-week MA), up (8.1%) YTD/YTD and have been on the rise for 7 of the last 13 weeks.

Note On the Color Codes

Banner colors reflect an assessment of the current conditions in the overall economy and the business chemistry of chemistry. For the overall economy we keep a running tab of 20 indicators. The banner color for the macroeconomic section is determined as follows:

Green – 13 or more positives

Yellow – between 8 and 12 positives

Red – 7 or fewer positives

There are fewer indicators available for the chemical industry. Our assessment on banner color largely relies upon how chemical industry production has changed over the most recent three months.

For More Information

ACC members can access additional data, economic analyses, presentations, outlooks, and weekly economic updates through ACCexchange: https://accexchange.sharepoint.com/Economics/SitePages/Home.aspx

In addition to this weekly report, ACC offers numerous other economic data that cover worldwide production, trade, shipments, inventories, price indices, energy, employment, investment, R&D, EH&S, financial performance measures, macroeconomic data, plus much more. To order, visit http://store.americanchemistry.com/.

Every effort has been made in the preparation of this weekly report to provide the best available information and analysis. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.

Contact us at ACC_EconomicsDepartment@americanchemistry.com.