MACROECONOMY & END-USE MARKETS

Running tab of macro indicators: 14 out of 20

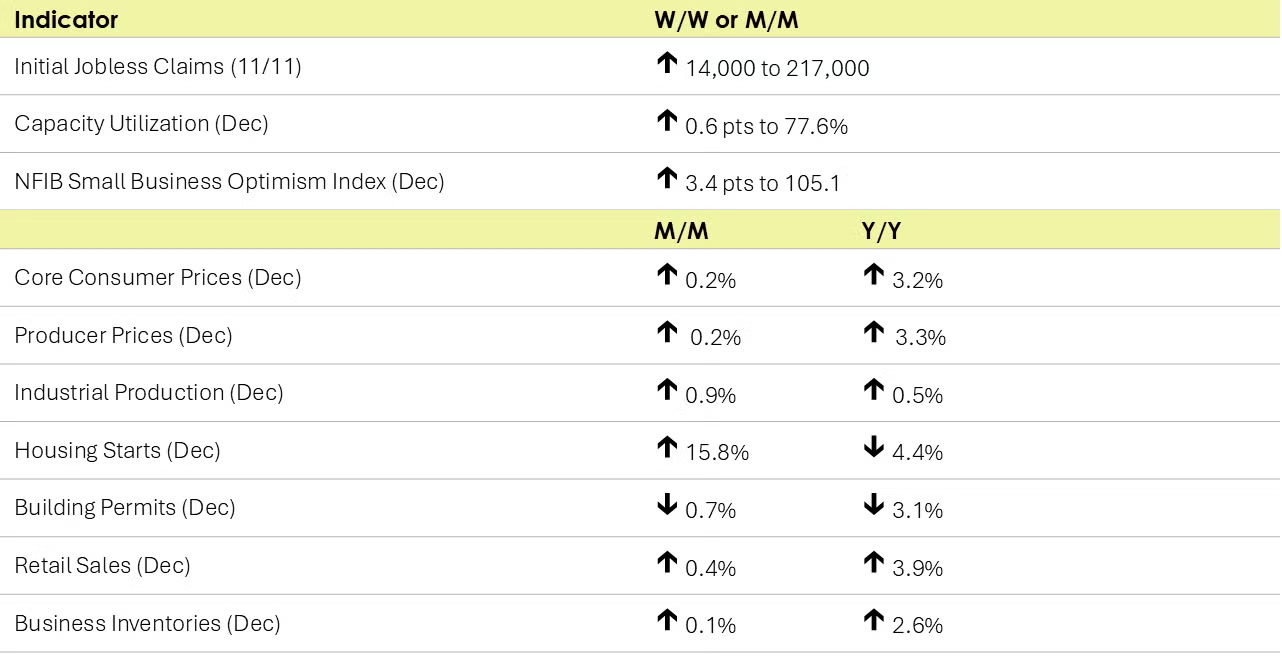

The number of new jobless claims rose by 14,000 to 217,000 during the week ending January 11. Continuing claims fell by 18,000 to 1.859 million, and the insured unemployment rate for the week ending January 4 was unchanged at 1.2%.

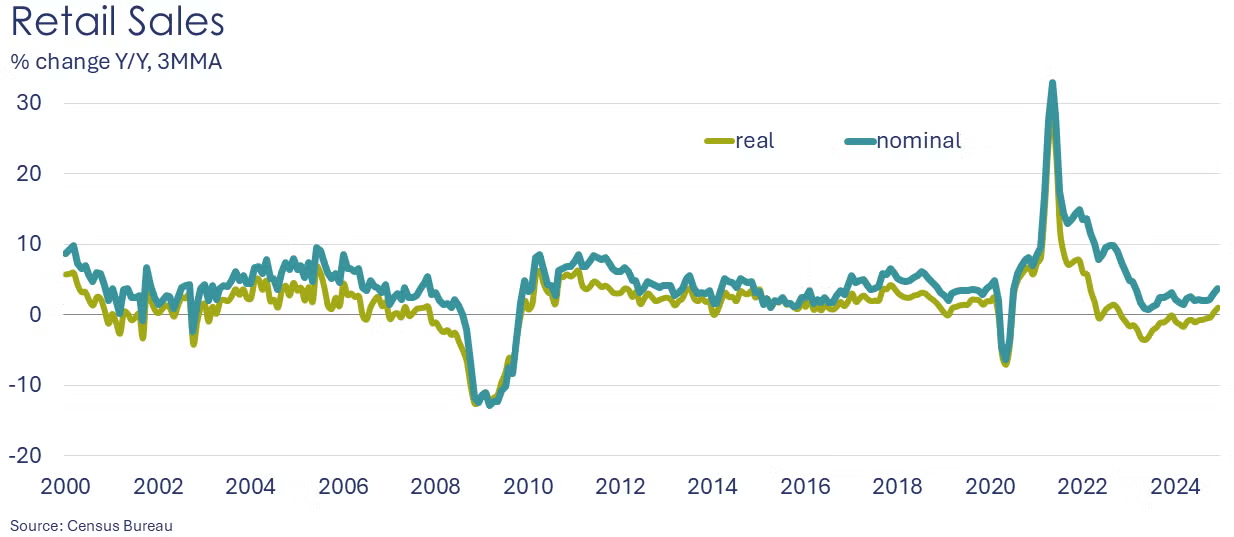

Headline retail and food service sales rose 0.4% in December. Gains were broad based with a few exceptions. Sales at building materials and garden centers fell for a third month and restaurant sales fell for the first time in nine months. Compared to last December, retail sales were up 3.9% Y/Y.

Consumer prices (as measured by the consumer price index, or CPI) rose 0.4% in December, the largest monthly jump since February. The gain was driven by higher gasoline prices which accounted for 40% of the increase in the headline CPI. Headline consumer prices rose 2.9% Y/Y (the third increase since September) while core consumer prices (excluding food & energy) were up 3.2% Y/Y, a slight decline compared to November.

Headline producer prices rose by 0.2% in December, led by strong gains in energy prices. Prices for core goods (excluding food & energy) were flat. On the services side, gains in prices for transportation and warehousing offset declining prices in trade and other services. Compared to a year ago, headline producer prices rose 3.3% (up from 3.0% in November). Core producer prices also rose 3.3% Y/Y, an improvement over the 3.5% annual pace in October and November.

U.S. import prices edged up slightly (0.1%) in December and were up 2.2% Y/Y. Import fuel prices advanced 1.4% in December following a 0.9% gain the previous month. Higher prices for natural gas and petroleum contributed to the increase in import fuel prices. Prices for import fuel rose 0.3% over the past 12 months. Excluding fuel, nonfuel import prices also rose in December. Export prices rose 0.3% in December and were up 1.8% Y/Y. Prices for agricultural exports rose 0.5% and non-agricultural exports prices were up 0.3%.

Combined business inventories edged slightly higher in November (up 0.1%). There were gains in retail and manufacturers’ inventories and a decline in wholesalers’ inventories. Business sales rose 0.5% as gains occurred for retailers, manufacturers and wholesalers. Business inventories were up 2.6% Y/Y while sales were higher by 2.5% Y/Y. The inventories-to-sales ratio remained steady at 1.37. A year ago, the ratio was 1.37.

Housing starts surged in December, up by 15.8% to their highest pace since February. The gain reflected a nearly 60% gain in permits for large multifamily projects (5+ units). Starts for single-family homes were also higher, with gains in all regions, except the South which was flat. Forward-looking building permits eased, however, down 0.7%, led by declines in permits for multifamily structures. Compared to a year ago, overall housing starts were off 4.4% Y/Y while building permits were down 3.1% Y/Y.

Led by growth in the Americas, global semiconductor sales rose 1.6% in November to $57.82 billion and were up 20.7% Y/Y.

Small business optimism improved in December up by 3.4 points to 105.1, according to the National Federation of Independent Businesses (NFIB). The largest gain was in expectations for the economy to improve. The Uncertainty Index declined sharply, as business owners became more certain about economic policies following the election. Inflation remained the most important problem for small businesses.

Industrial production rose for a second month in December, up 0.9%. Manufacturing output posted its highest monthly gain since May. Utility output was also higher, but mining output continued to ease. The gain in manufacturing output was led by aerospace which rose sharply following the conclusion of the two-month Boeing strike in early-November. There were also large gains in the output of primary metals, fabricated metal products, printing, petroleum products and apparel. Output of motor vehicles, computers & electronics, and nonmetallic mineral products were among the industries that saw lower production.

Compared to a year ago, overall industrial production was up 0.5%. Capacity utilization also rose, up 0.6 points to 77.6%. Capacity utilization was slightly below its 78.1% rate a year ago. Over the past year, overall industrial capacity has grown by 1.2% Y/Y.

Looking into January, regional manufacturing surveys were mixed. According to the Empire State Manufacturing Survey, business activity weakened in New York State with shipments and new orders declining. In the Philadelphia Federal Reserve district, manufacturing increased overall in January. Its headline general business index jumped from a reading of -10.9 to 44.3 in December. Shipments, new orders, and employment increased. Inventories rose and unfilled orders were higher. Looking ahead, manufacturers remained optimistic and is building.

FED BEIGE BOOK

- Economic activity increased slightly to moderately across the twelve Federal Reserve Districts in late November and December.

- Consumer spending moved up moderately, with most Districts reporting strong holiday sales that exceeded expectations.

- Vehicle sales grew modestly.

- Construction activity decreased overall, with several Districts indicating that high costs for materials and financing were weighing on growth.

- Manufacturing decreased slightly on net, and a number of Districts said manufacturers were stockpiling inventories in anticipation of higher tariffs.

- Residential real estate activity was unchanged on balance, as high mortgage rates continued to hold back demand. The nonfinancial services sector grew slightly overall, with Districts highlighting growth in leisure and hospitality and transportation, notably air travel.

- Truck freight volumes, however, were down.

- Agricultural conditions remained weak overall, with generally lower farm incomes and weather-related struggles in some areas. The spread of avian flu reduced egg supplies and pushed up prices.

- Energy activity was mixed.

- More contacts were optimistic about the outlook for 2025 than were pessimistic about it, though contacts in several Districts expressed concerns that changes in immigration and tariff policy could negatively affect the economy.

ENERGY

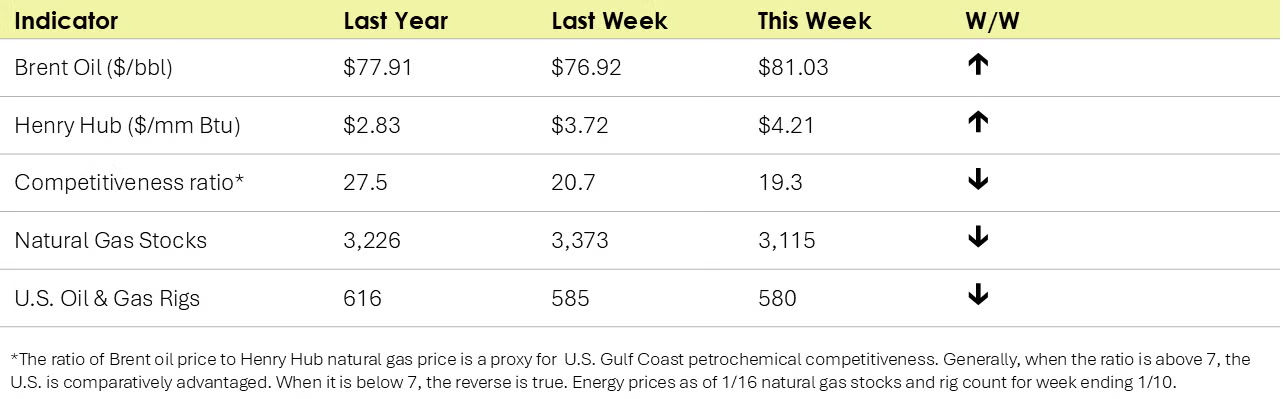

- Oil prices were higher than a week ago following new sanctions on Russian oil, but lower today following the ceasefire announcement in Gaza that triggered expectations for a halt in Houthi shipping attacks in the Red Sea.

- U.S. natural gas prices blew past $4/mmbtu as a polar vortex is forecast for next week. Last week saw the largest withdrawal from inventories (258 BCF) in nearly a year. Inventories remained within their historic range, however.

- The combined oil & gas rig count fell by five to 580.

CHEMICALS

Indicators for the business of chemistry suggest a yellow banner.

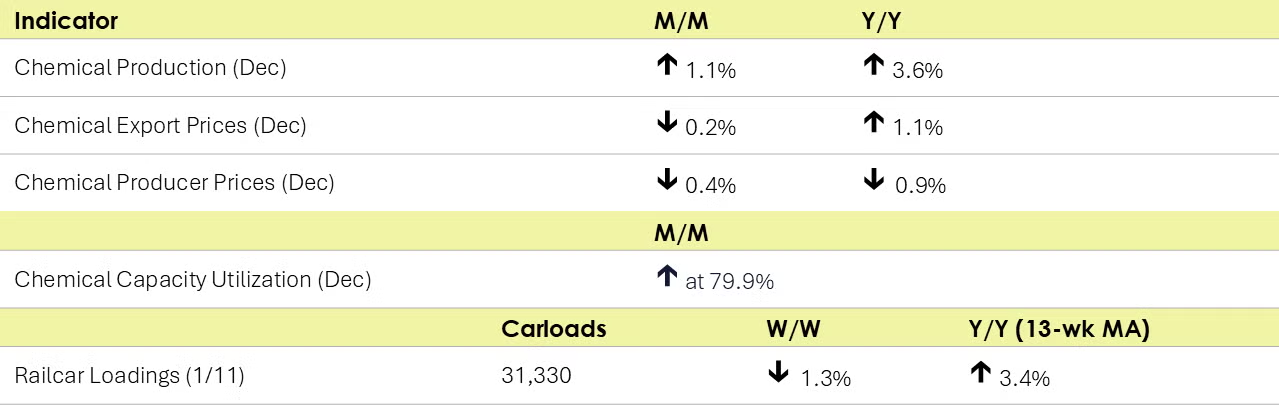

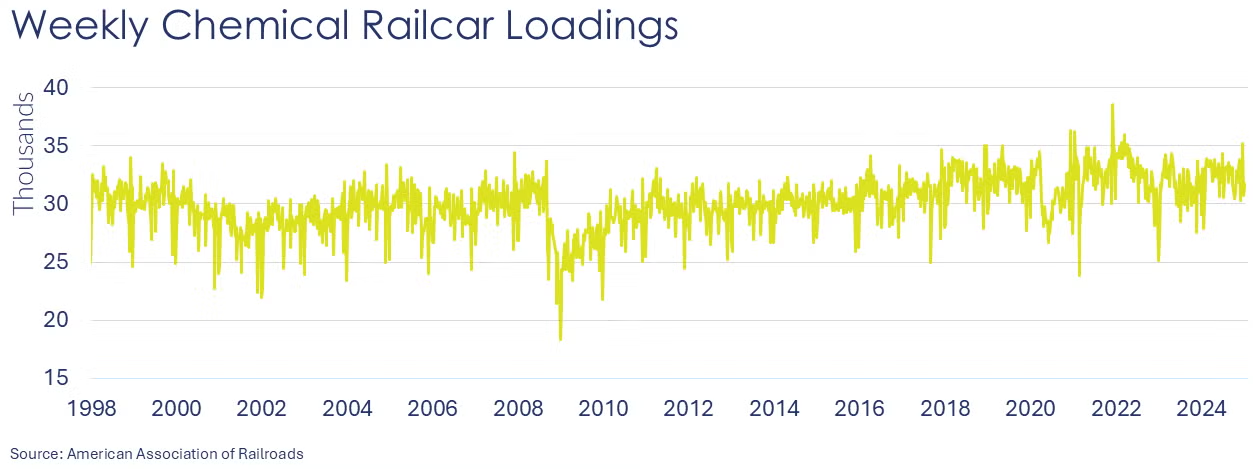

According to data released by the Association of American Railroads, chemical railcar loadings were down to 31,330 for the week ending January 11. Loadings were up 3.4% Y/Y (13-week MA), up (1.5%) YTD/YTD and have been on the rise for 7 of the last 13 weeks.

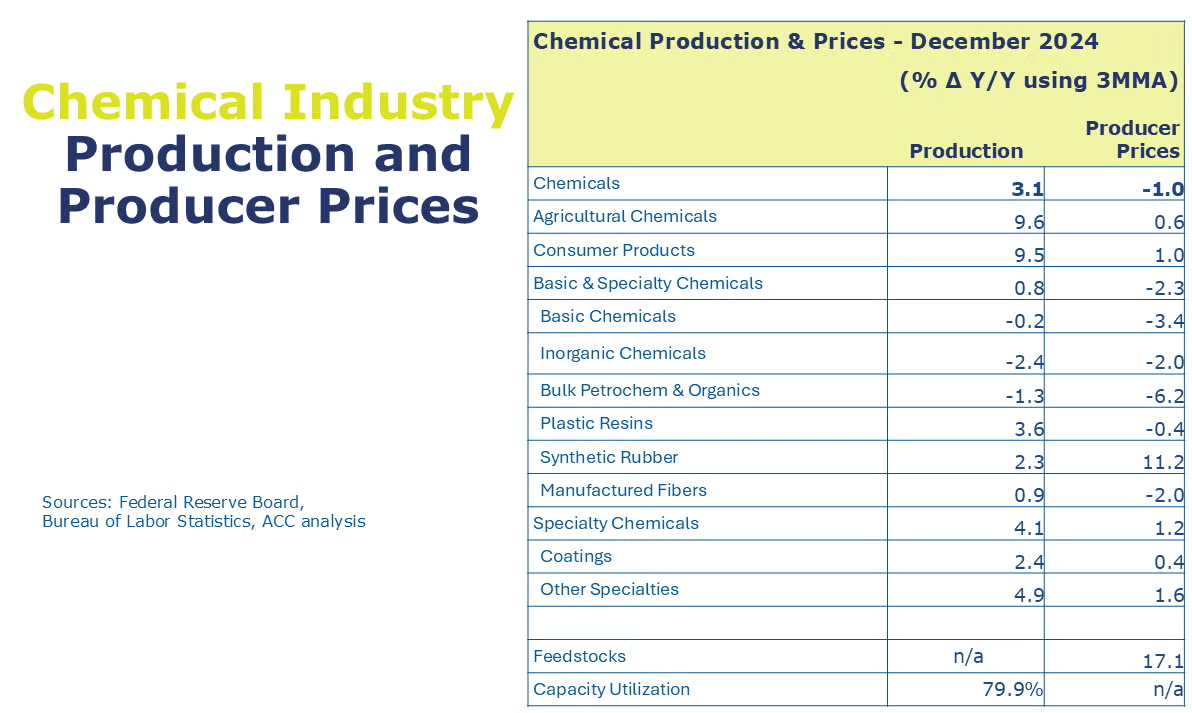

Chemical production finished the year strong. Output of chemicals rose for a third consecutive month, up by 1.1%. Gains were broad based except for a pullback in the production of synthetic materials (including plastic resins, synthetic rubber, and manufactured fibers) and consumer products. The strongest gains were in organic chemicals, coatings, adhesives, other specialty chemicals, crop protection chemicals and industrial gases. Chemical capacity utilization rose sharply from 79.0% in November to 79.9% in December, its highest since March 2022.

Chemical producer prices slipped for a fifth straight month in December, down another 0.4%. Compared to a year ago, overall chemical prices were 0.9% lower. In December, prices were lower for organic chemicals, plastic resins, synthetic rubber, coatings, and other specialty chemicals. Those declines were partially offset by higher prices for agricultural chemicals and manufactured fibers. Prices for inorganic chemicals and consumer products were flat. Feedstock costs were up 10.0% in December and were up 21.8% Y/Y.

Prices for imported chemicals fell 0.1% in December and were down 1.8% Y/Y. Prices for chemical exports fell 0.2% and were up 1.1% Y/Y.

Note On the Color Codes

Banner colors reflect an assessment of the current conditions in the overall economy and the business chemistry of chemistry. For the overall economy we keep a running tab of 20 indicators. The banner color for the macroeconomic section is determined as follows:

Green – 13 or more positives

Yellow – between 8 and 12 positives

Red – 7 or fewer positives

There are fewer indicators available for the chemical industry. Our assessment on banner color largely relies upon how chemical industry production has changed over the most recent three months.

For More Information

ACC members can access additional data, economic analyses, presentations, outlooks, and weekly economic updates through ACCexchange: https://accexchange.sharepoint.com/Economics/SitePages/Home.aspx

In addition to this weekly report, ACC offers numerous other economic data that cover worldwide production, trade, shipments, inventories, price indices, energy, employment, investment, R&D, EH&S, financial performance measures, macroeconomic data, plus much more. To order, visit http://store.americanchemistry.com/.

Every effort has been made in the preparation of this weekly report to provide the best available information and analysis. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.

Contact us at ACC_EconomicsDepartment@americanchemistry.com.