Looking into 2025, a mix of challenges and opportunities will emerge for US chemical producers.

“Looking into 2025, a mix of challenges and opportunities will emerge for US chemical producers,” said Martha Moore, Chief Economist at the American Chemistry Council. “Against the backdrop of new political leadership, weak global demand and production from China, the U.S. chemical industry looks forward to building on its energy advantage to become increasingly competitive in a changing global market.

Economic Outlook

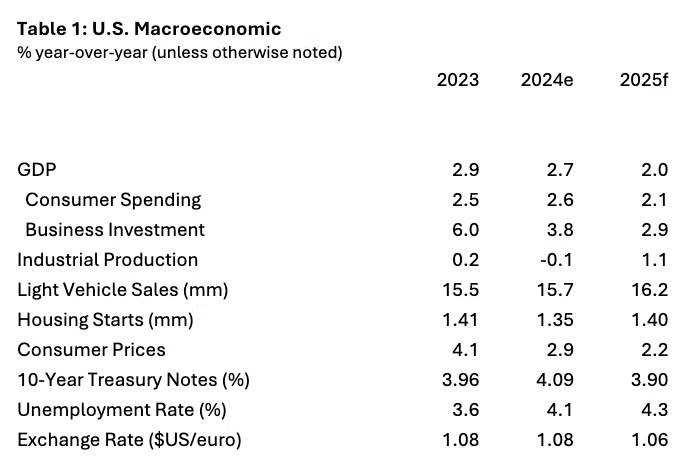

With the beginning of an interest rate cutting program by the Federal Reserve in September, recession risks have lessened and the U.S. economy is on solid ground heading into the end of 2024. Inflation continues to ease, but slowly. A tight labor market has kept pressure on wage growth, which remains above average and has supported consumer spending. Investment, especially in equipment, has been robust. Large segments of the manufacturing sector remain weak however. We expect U.S. GDP will have risen 2.7% in 2024, before slowing to a 2.0% gain in 2025.

Inflation continued to decrease in 2024, but progress has remained slow. The trend in the Fed’s target, the price index for core personal consumption expenditures, has remained stable since Q2. Across the various measures of inflation, it is clear that inflation in services continues to exceed price growth for goods. Indeed, many goods prices have declined over the past year due to weak demand and overcapacity in some segments. Headline consumer prices rose 2.9% in 2024 (down from 4.1% in 2023) and are expected to drift lower to 2.2% in 2024.

The Fed initiated its first rate cut in more than four years in September and cut rates again in November. Lower borrowing costs are expected to encourage investment and consumption, though there is a lag. Price pressures from tariffs and wage growth, however, could create challenges to the Fed’s interest rate cutting program.

Consumer spending remained resilient in 2024 supported by wage gains and a historically tight (though cooling) labor market, which enables consumers’ ability to spend. Consumer spending is performing slightly better than last year. We expect consumer spending to rise 2.6% in 2024, up from 2.5% in 2023. As the labor market continues to cool, wage growth will ease, and growth consumer spending is expected to slow to a 2.1% pace in 2025.

Business investment, motivated, in part, by recent legislation (e.g., Inflation Reduction Act, CHIPS Act) and re- and near-shoring activity, rose by a revised 6.0% in 2023. With higher borrowing costs and tighter credit conditions, growth business investment slowed in 2024 (to 3.8%), but came in better than expected earlier in the year. Spending on equipment, in particular, was especially strong. We expect business investment growth to slow in 2025 to 2.9%.

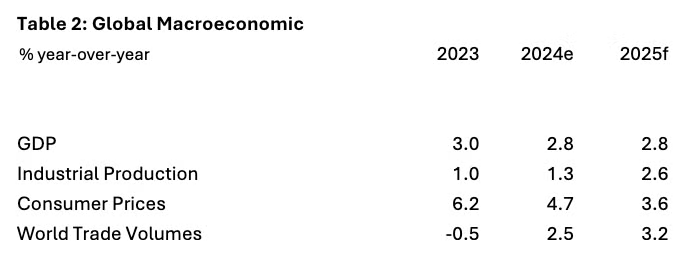

The global economy is expected to grow by 2.8% this year. The expansion will likely be supported by better-than-expected performance in the US economy, in addition to strong gains in India. Global GDP is forecast to increase at a steady 2.6%-2.8% pace through the end of our forecast period (2032).

Industrial activity continued to be weak worldwide, with only a modest recovery in 2024. Global industrial production growth is forecast to increase by 1.3% this year (2024) before accelerating to 2.6% growth in 2025.

Following a small contraction in 2023, world trade volumes should recover modestly, growing at a 2.5% pace this year (2024) before accelerating slightly to a 3.2% pace in 2025.

Chemical Demand Remained Weak – Modest Recovery in 2025

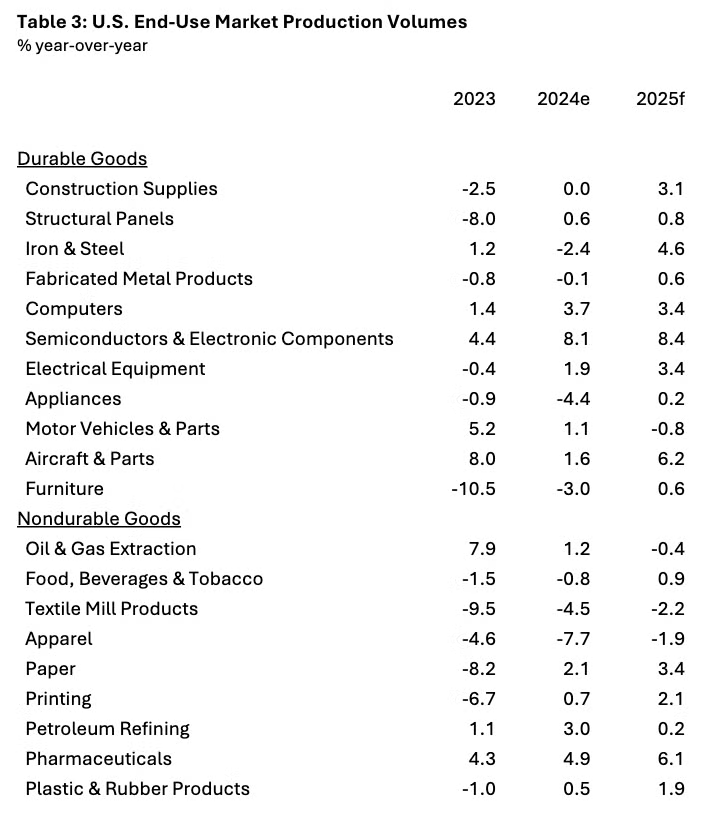

More than 80% of basic and specialty chemicals are consumed by the industrial sector and industrial production stalled in 2024 following essentially stagnant growth in 2023. Demand in the U.S. and abroad was hampered by strikes, supply chain disruptions, and several hurricanes. Overall industrial production is expected to be flat (down 0.1%) for a second consecutive year in 2024. As interest rates continue to fall and growth expectations in key customer economies improve in the U.S. and abroad, we expect a slight improvement in 2025 (up 1.1%).

Having contracted in 23 of the past 24 months, the ISM Manufacturing PMI® suggests manufacturing activity has remained weak overall. Within manufacturing, performance among sectors has been uneven. In 2023, only eight of the 20 key chemistry end-use industries we track expanded. There was an improvement in 2024 with 12 of the 20 expanding. Industries tied to semiconductors, computers, and electrical equipment did well, while industries linked to construction (e.g., structural panels, appliances, and furniture) remained weak. In 2025, we expect growth in 16 of the 20 industries.

One of the most important end-use markets for chemistry is automobiles. The average automobile built in North America contains more than $4,400 of chemistry products (including 426 lbs. of lightweight and durable plastics and composites). Despite four years of below-average sales, vehicle sales face affordability constraints as dealer inventories remain tight. The total cost of vehicle ownership (including purchase prices, borrowing costs, insurance, maintenance, and repair) has escalated. Growth in vehicle sales is expected to move slightly higher to 15.7 million in 2024 and 16.2 million in 2025.

With 33,000 pounds of chemistry products in the average single-family home built in the U.S., another important end-use market for chemistry is housing. Interest rate-sensitive housing continued to struggle in 2024. Low inventories of existing homes (due in part to mortgage rate differentials which have kept many existing homeowners locked in) kept pressure on home prices. In the existing home market, which is linked to home remodeling activity, 2024 was likely the worst year since 1995. New homebuilding was also challenged by land-use regulations and labor shortages. Housing starts fell to 1.35 in 2024 but are expected to rise slightly to 1.40 in 2025 as interest rates begin to ease.

Chemical Production Eased Again in 2024

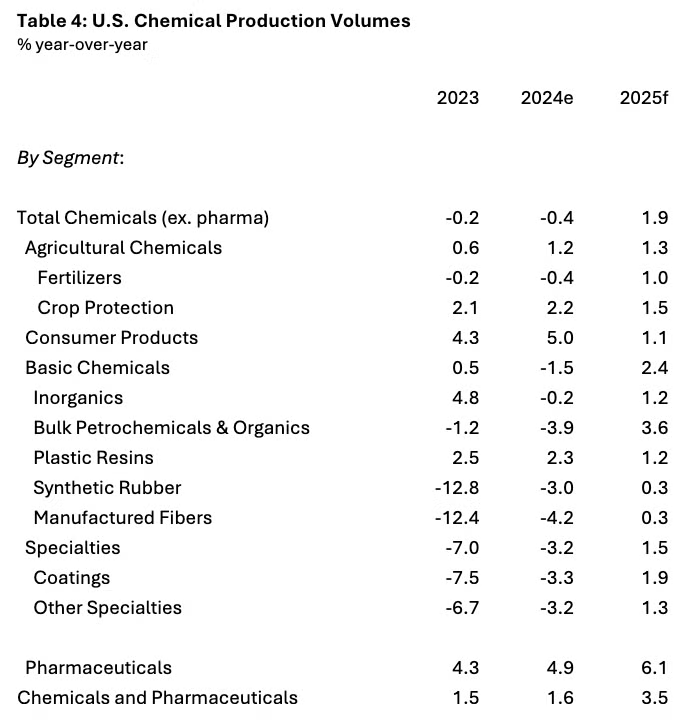

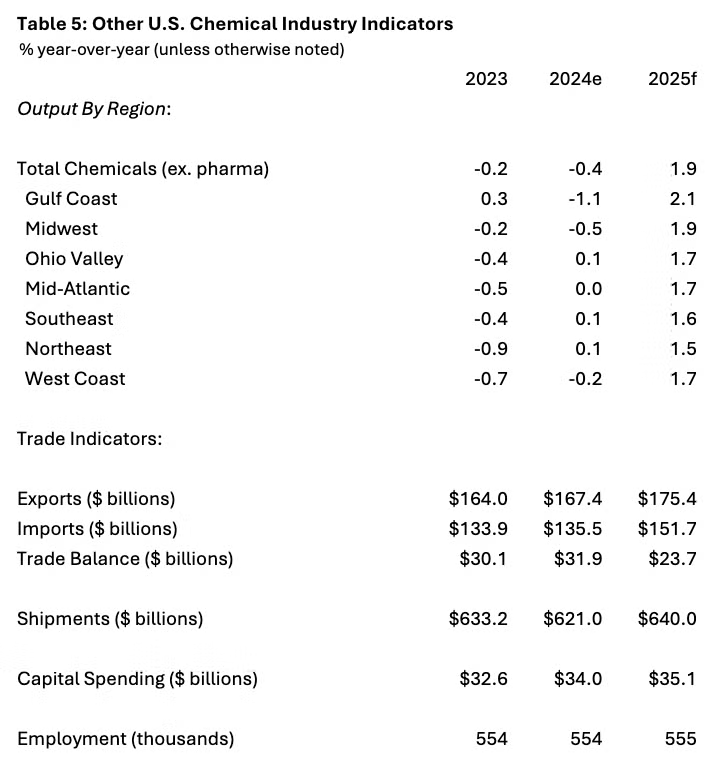

While the unprecedented destocking cycle has played out, the ongoing weak demand for manufactured products in the U.S. and abroad continues to challenge the U.S. chemical industry. While chemical production remained largely unchanged in 2023, off by 0.2%, output eased again in 2024, as many chemistry-consuming end-use markets remained depressed. As a result, we expect chemical output volumes to fall 0.4% in 2024 with gains in agricultural chemicals and consumer products offsetting declines in basic & specialty chemicals. On the higher industrial tide driven by the impact of lower interest rates on investment and consumption, chemical output is expected to grow 1.9% in 2025. Within the U.S., the largest gains are likely to emerge in the Gulf Coast and Midwest regions next year.

Indeed, industrial production and capacity utilization for chemicals improved in Q3. This is consistent with the findings of ACC’s Economic Sentiment Index that found chemical firms felt that overall business activity improved slightly in Q3 and is expected to increase over the next six months.

Amid weak demand, output of basic chemicals in the U.S. fell by 1.5% in 2024 with gains in plastic resin output offsetting declines in organic and inorganic chemicals, in addition to synthetic rubber and manufactured fibers. Plastic resins output is predicted to grow, up 2.3% in 2024, in part due to competitive exports. Specialty chemical output is also expected to fall again in 2024, by 3.2%, reflecting the slow recovery across many end-use markets. Output of agricultural chemicals is expected to rise 1.2% with a gain in the output of crop protection chemicals offsetting a small decline in fertilizers. Production of consumer products, which grew strongly last year accelerated by 5.0% this year. In 2025, we expect gains across all segments, in line with a modest recovery across construction and manufacturing. Agricultural chemicals and consumer products is expected to also continue to expand by 1.3% and 1.1% respectively.

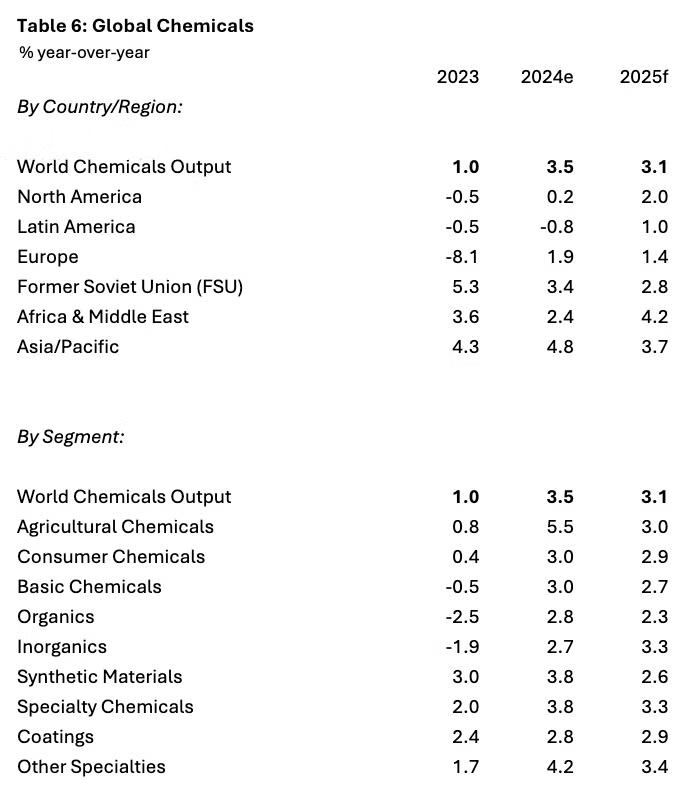

Globally, chemical production is expected to expand by 3.5% in 2024 with gains across most regions. The largest gains were in Asia/Pacific, former Soviet Union economies and Africa & Middle East. Output in Europe expanded following a steep decline in 2023 as energy prices surged in response to Russia’s invasion of Ukraine. Latin America is the only region that is seeing contraction as some countries are struggling with high inflation and low productivity while others did not leverage friendshoring opportunities and struggle with structural issues. Growth should continue into 2025 with global volumes up by 3.1%.

Chemical Trade on the Rise

Trade is vital to the U.S. chemical industry. As the 2nd largest manufacturing exporter, the chemical industry has maintained a trade surplus for decades . Nearly 200,000 chemical industry jobs depend on exports of chemicals and other U.S. manufactured goods. U.S. chemicals exports are projected to rise 2.1% this year (2024) following a decline over 2023. U.S. chemical imports are also projected to rise this year, growing by 1.2%. Chemical exports will average about 4-5% annually over our forecast period while imports are expected to average a 7% annual pace of growth subject to potential changes in trade policy. The U.S. continues to maintain a trade surplus in chemicals throughout the forecast horizon.

Capital Spending Grows

Growth in capital spending remained strong in 2024 despite higher borrowing costs. In 2024, spending on capital projects rose 4.1% to $34 billion. Between 2025 and 2028, capex is expected to grow on average by 2.9% per year. While some investment continues in shale-advantaged projects, there have been new investments in specialty chemicals to support growing capacity for semiconductors, batteries, etc. Investment activity related to sustainability also remains an active space.

Employment Stays Flat

Following strong gains in 2022, chemical industry employment eased slightly in 2023 and will come in essentially flat in 2024. Chemical industry employment bottomed out in Q1 2024 and rose in Q2 and Q3. Chemical industry employment is expected to expand slowly in 2025 (by 0.2%) with slow gains through 2027.

Longer-Term Outlook & Opportunities for Enhanced Competitiveness

The longer-term outlook for U.S. chemistry remains positive with the natural gas liquids feedstock advantage continuing to favor U.S. production for the foreseeable future. Capacity expansions in customer industries motivated by recent legislation (e.g., IRA, IIJA, CHIPS) will also create demand for U.S. chemistry. For example, semiconductor manufacturing requires 500 different process chemicals and electric vehicles have a higher polymer content than ICE vehicles. A recent surge of manufacturing investment in Mexico (one of the industry’s top destinations for U.S. chemical exports) also has the potential to boost demand for U.S.-made chemistry.

The incoming administration has the opportunity to craft policies to enhance the competitiveness of the U.S. chemical industry, including tax reforms, chemical management regulations, and actions to protect the U.S. industrial base from illegal trade practices.

As with any outlook, there are variables that could alter the projected outcomes. A “higher for longer” interest rate policy by the Fed could dampen demand. In addition, policies that create broad trade barriers could be harmful to U.S. chemical manufacturing. In addition, new or escalating geopolitical conflicts, unexpected financial volatility, external shocks (i.e., weather, cyberattack, etc.) could also disrupt this outlook.

The full data set with historic trends and forecasts through 2027 is available to ACC members on ACCExchange and to others on the ACC Store.

Reasonable effort has been made in the preparation of this publication to provide the best available information. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.