Running tab of macro indicators: 13 out of 20

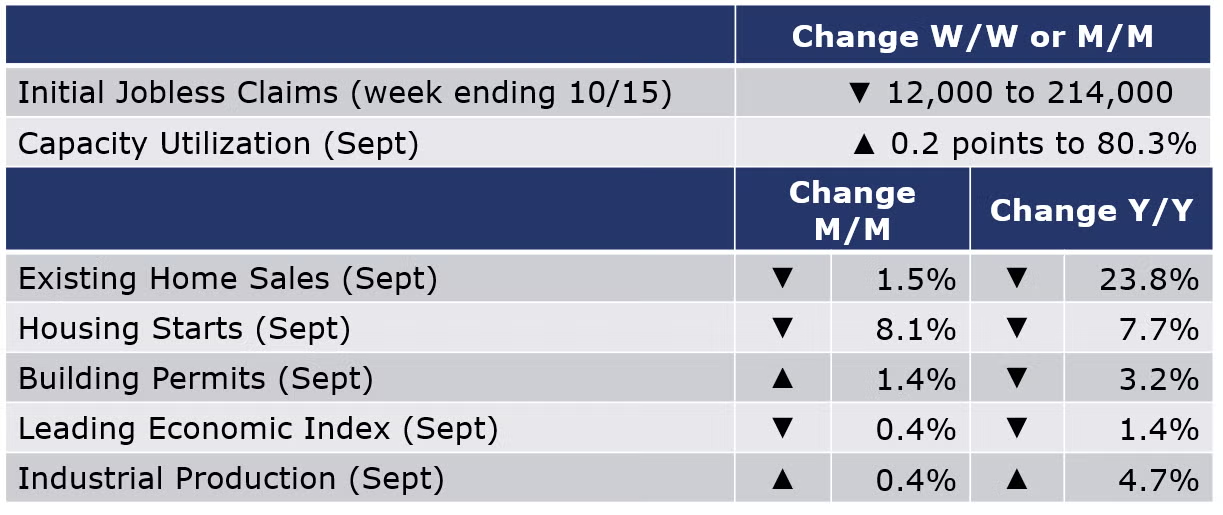

The number of new jobless claims was down by 12,000 to 214,000 during the week ending 15 October. Continued claims were up 21,000 to 1.385 million for the week ending October 8th and the insured unemployment rate was 1.0%, virtually unchanged from the previous week's revised rate.

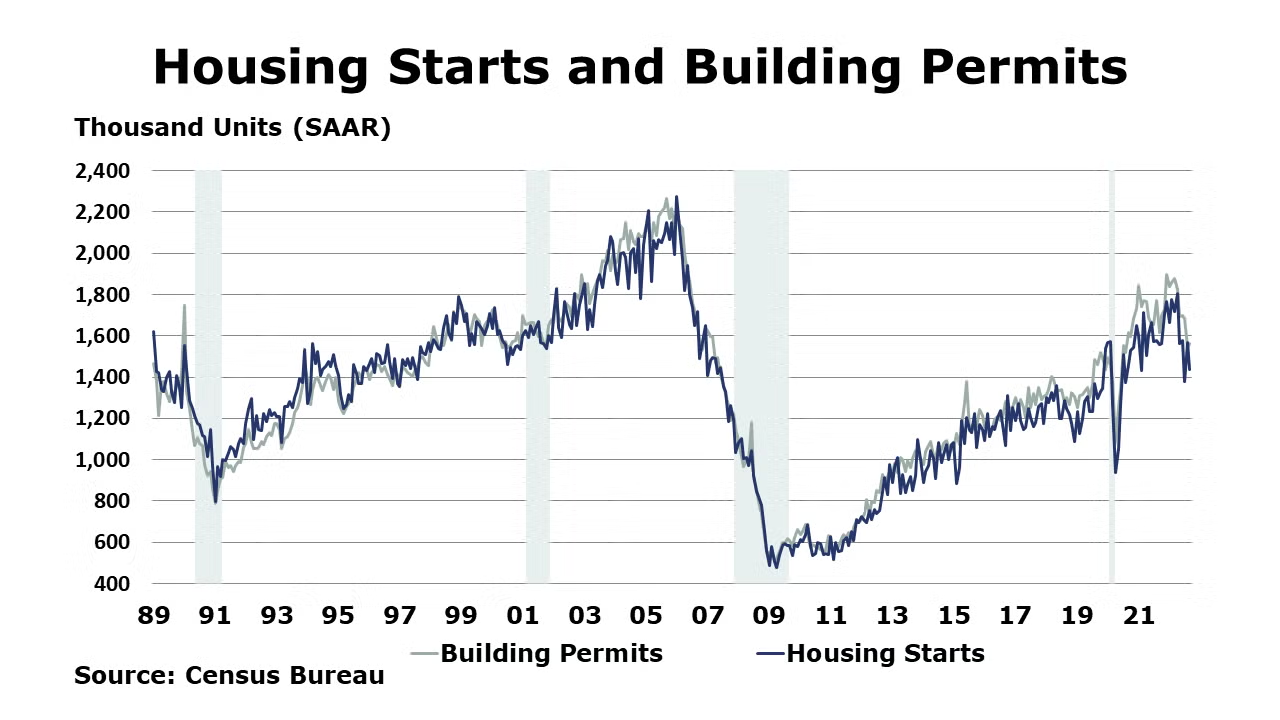

Total housing starts declined in September by 8.1% to a 1.44 million pace after a brief jump in August. The level remains below the cycle peak in December 2021 and 7.7% below the September 2021 level. Most regions posted declines this month with the exception of the West region, where housing starts increased. Forward-looking building permits, however, rose 1.4% to 1.56 million units on a seasonally adjusted at annual rate basis with all regions recording gains except the Northeast. Single-family units showed a decline that was more than made up by multi-family units. Rising mortgage rates will continue to exert downward pressure on construction activities going forward.

Existing home sales fell 1.5% in September to a 4.71 million seasonally adjusted annual pace, a rate 23.8% lower than a year ago. At the end of August, inventories stood at 1.25 million homes for sale or under contract. which is down 2.3% from July and 0.8% from a year earlier. The level of inventories represents a lean 3.2-month supply. With historically lean inventories, the median sales price moderated slightly but is still up 8.4% from a year ago to $384,800.

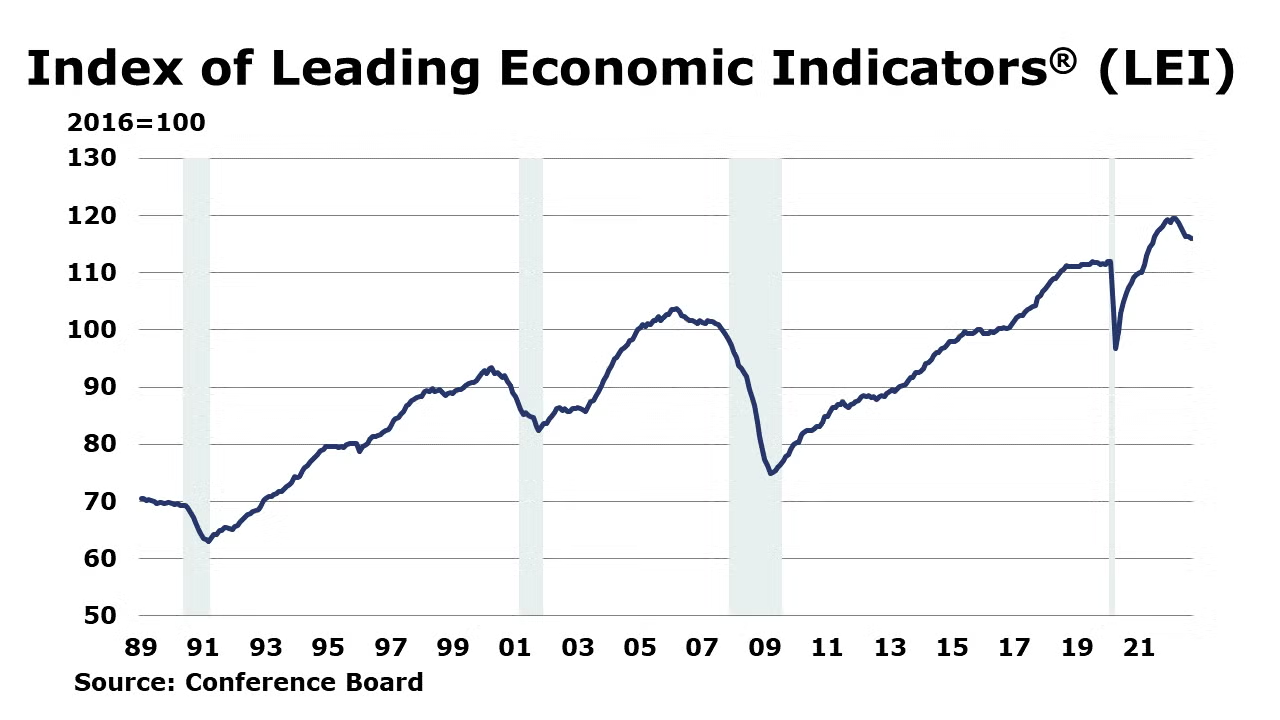

The Conference Board’s Leading Economic Index® (LEI) fell 0.4% in September. The LEI has declined persistently in recent months. The decline to 115.9 was the seventh consecutive decline. The index was down 2.8% over the previous six months, a reversal of the 1.4% growth over the previous six-month period. The LEI was off 1.4% Y/Y, the second annual decline since early-2021. The Conference Board projects a recession is likely by year-end.

Industrial production rose by 0.4% in September. This is the fourth consecutive month of positive showings since June. Utility output was lower, but both mining and manufacturing output rose. Within manufacturing, the gains were recorded in nonmetallic mineral products, fabricated metal products, computer and electronic products, motor vehicles and parts, food, beverage, and tobacco products, apparel and leather, chemicals, and petroleum and coal products. The only two segments showing a decline were printing and miscellaneous manufacturing. Compared to a year ago, manufacturing output remained higher by 4.7%, while overall industrial production was up 5.3% Y/Y. Capacity utilization increased from 80.1% in August to 80.3%. A year ago, capacity utilization was 77.4%. Overall industrial capacity has grown 1.5% Y/Y.

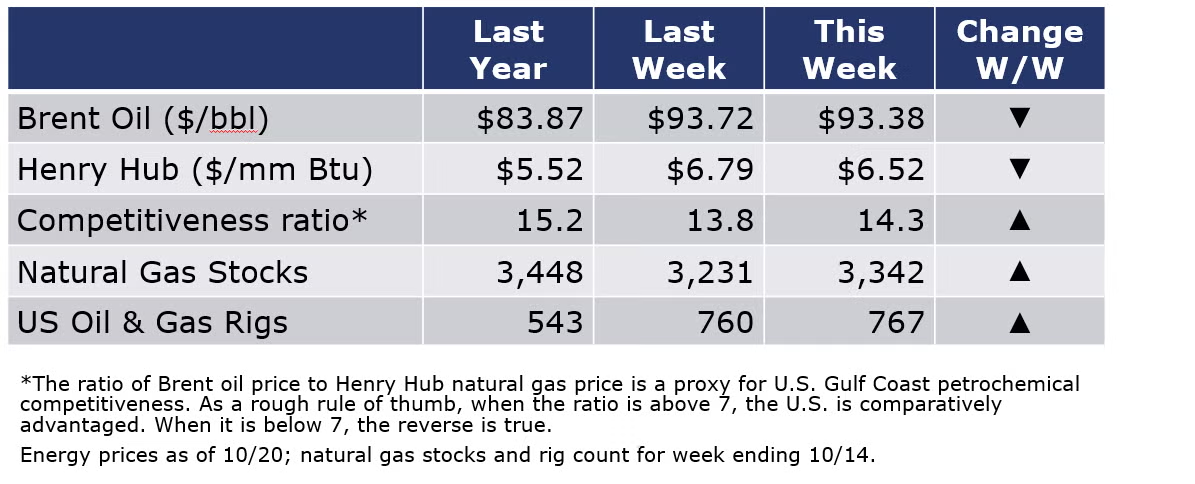

Oil prices declined slightly during the week and U.S. natural gas prices also fell. As a result, the oil to gas price ratio increased to 14.3. The ratio of Brent oil price to Henry Hub natural gas price is a proxy for U.S. Gulf Coast petrochemical competitiveness. As a rough rule of thumb, when the ratio is above 7, the U.S. is comparatively advantaged. When it is below 7, the reverse is true. The combined oil and rig count rose by seven to 767 during the week ending 10/14.

For the business of chemistry, the indicators still bring to mind a yellow banner for basic and specialty chemicals

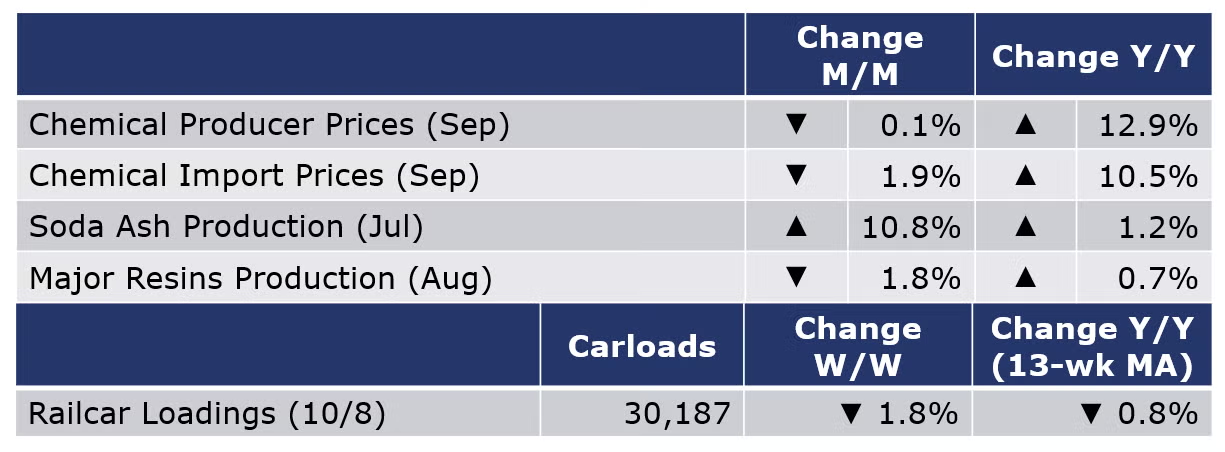

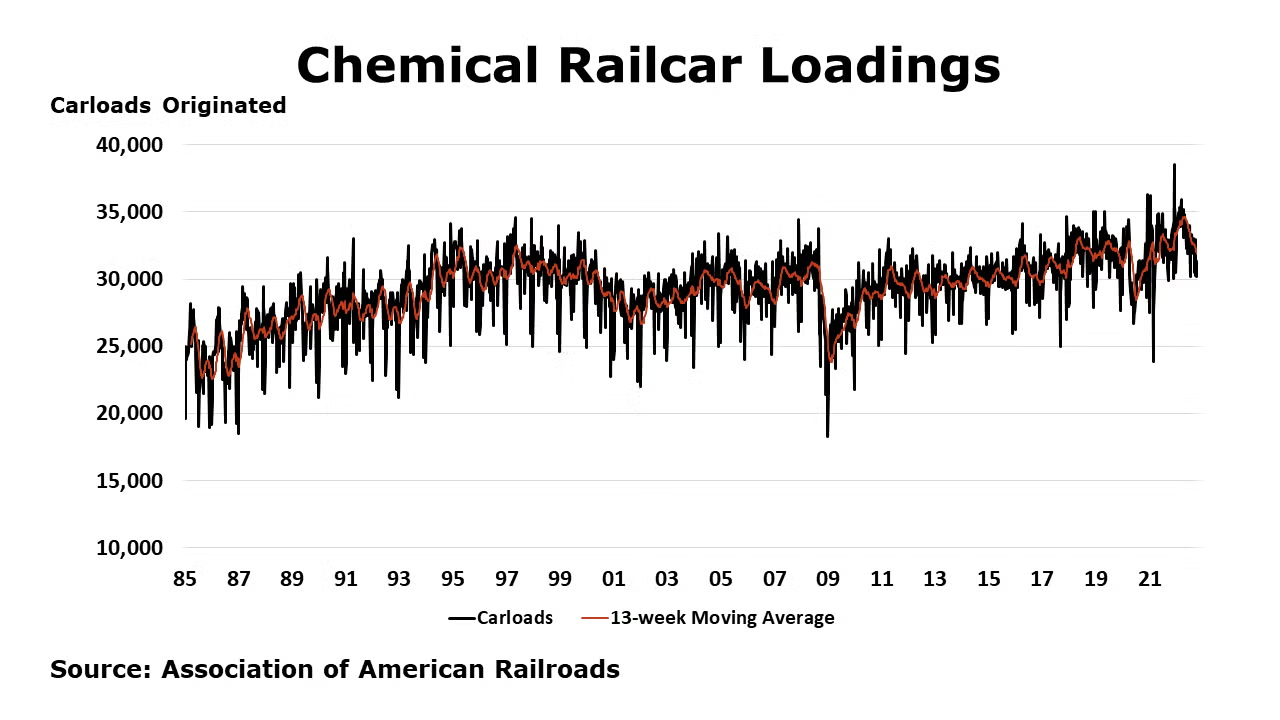

According to data released by the Association of American Railroads, chemical railcar loadings were up 3.6% to 31,288 during the week ending 15 October. Loadings were down 1.0% Y/Y (13-week MA), up 2.7% YTD/YTD and have been on the rise for six of the last 13 weeks.

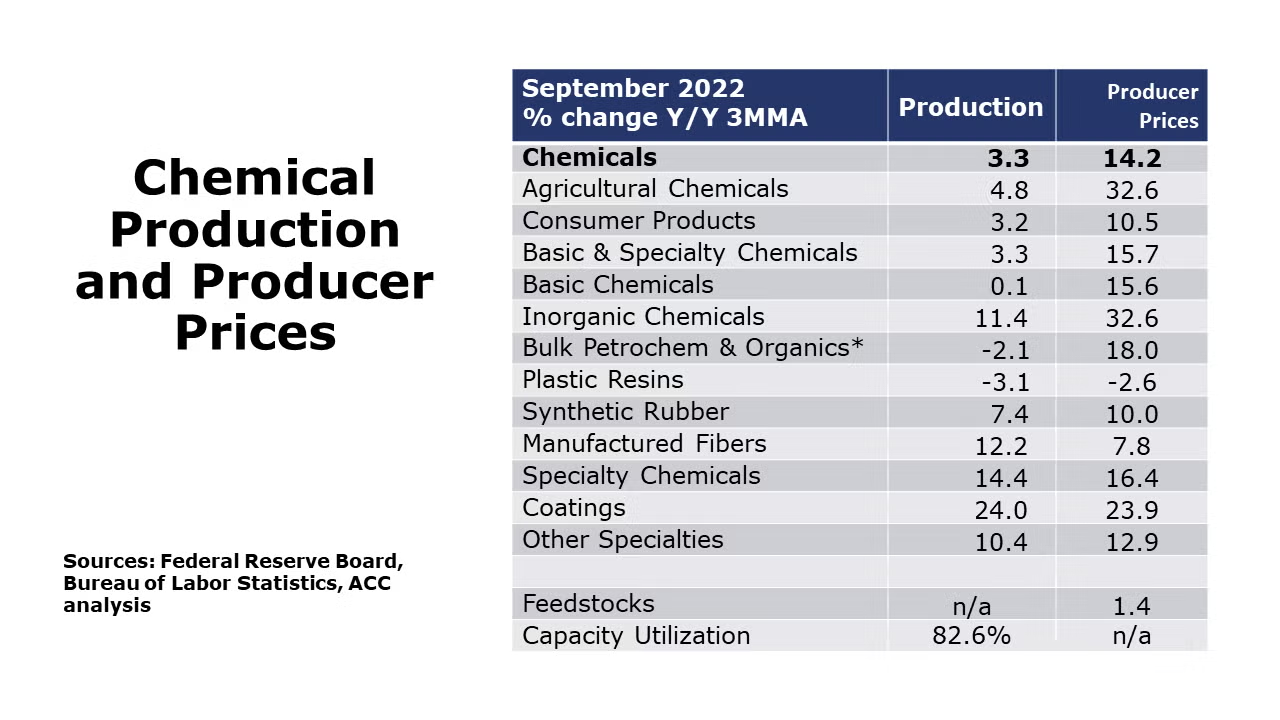

Chemical production remained stable in September with a 0% gain from the previous month. Performance was mixed with gains in the output of consumer products, coating, adhesives, fertilizers, and crop protection chemicals. Compared to a year ago, production remained ahead by 6.2% Y/Y. Chemical capacity utilization increased to 82.6% from 8.1% recorded last month, up from the 80.2% observed during the same month last year.

Note On the Color Codes

The banner colors represent observations about the current conditions in the overall economy and the business chemistry. For the overall economy we keep a running tab of 20 indicators. The banner color for the macroeconomic section is determined as follows:

Green – 13 or more positives

Yellow – between 8 and 12 positives

Red – 7 or fewer positives

For the chemical industry there are fewer indicators available. As a result we rely upon judgment whether production in the industry (defined as chemicals excluding pharmaceuticals) has increased or decreased three consecutive months.

For More Information

ACC members can access additional data, economic analyses, presentations, outlooks, and weekly economic updates through MemberExchange.

In addition to this weekly report, ACC offers numerous other economic data that cover worldwide production, trade, shipments, inventories, price indices, energy, employment, investment, R&D, EH&S, financial performance measures, macroeconomic data, plus much more. To order, visit http://store.americanchemistry.com/.

Every effort has been made in the preparation of this weekly report to provide the best available information and analysis. However, neither the American Chemistry Council, nor any of its employees, agents or other assigns makes any warranty, expressed or implied, or assumes any liability or responsibility for any use, or the results of such use, of any information or data disclosed in this material.

Contact us at ACC_EconomicsDepartment@americanchemistry.com